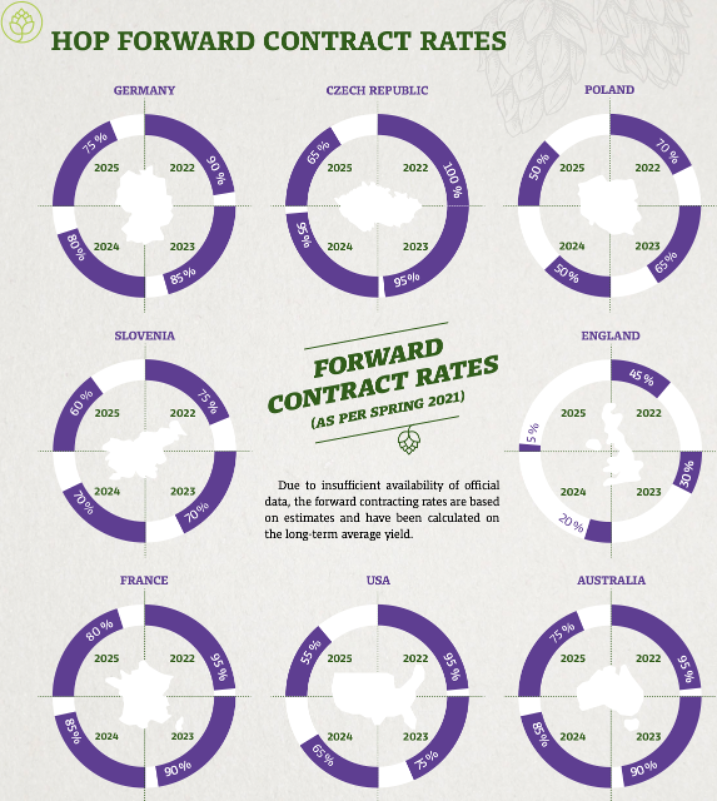

Based on the quantity of the crop reported as sold ahead in the recently released 2021/2022 BarthHaas report, it seems brewers have been busy signing forward contracts (Figure 1)[1]. These numbers are slightly down from just a few years ago. Hop contracts are encourage … marketed ... even pushed ... by farmers and merchants as if they are crucial to the existence of hops. That's because that’s what hop farmers and merchants need brewers to believe. But nothing is ever so black and white. There's a dark side to contracts I'd like to introduce you to.

Figure 1: BarthHaas Estimate on Industry Forward Contract Rates

Source: 2021/2022 BarthHaas Report

Hop Contracts … The Pros

It would not be fair to talk about the dark side of contracts without first discussing their positive benefits. The U.S. industry (particularly the states of Washington and Idaho) are a bell weather of the hop industry by which you can measure changes in the level of fear (among brewers) and opportunity (among growers). Farms in the Pacific Northwest (PNW), where nearly all U.S. hops are grown, are large corporations. Some of them make $50-100 million dollars and produce thousands of acres of hops each year. These farms rely on bank financing for their survival, which in turn looks to the value of assets and forward contracts for collateral. Behemoth American farms run on borrowed money. Forward contracts bring value to the American hop farm in that they enable the farmer and the merchant to go deeply into debt to produce the crop they have promised to deliver. That means without forward contracts, given the status quo, they cannot afford to produce the crop. We'll pull on that thread a little more in a bit.

Owners of many U.S. hop farms in the PNW have removed the bulk of their most valuable assets (think land and cash) from company ownership by placing them in separate entities to isolate them from risk. Forward contracts and the remaining assets farms own, which are still quite valuable, are the collateral available to the banks. In recent years, banks started including the value of picking machines as collateral whereas just 15-20 years ago those assets were considered worthless. If a buyer's market ever develops again, those assets would likely be considered worthless again. What value do extra picking machines have when there's a surplus of hops?

So, forward contracts enable U.S. hop farming entities to borrow money. With that money, they can increase their infrastructure faster than the market would otherwise allow. Farmers in Washington and Idaho respond quickly to changing market conditions. Over the past decade alone, they doubled acreage in response to increased demand[2]. Washington and Idaho are the only two places ... in the world ... where farmers can plant hops in the spring and harvest a reasonable crop in the fall under normal weather conditions ... hence their bell weather status as I mentioned above ... and they're both in the PNW of the United States. All other hop producing countries wait up to three years to harvest their first crop. How's that for a competitive advantage?

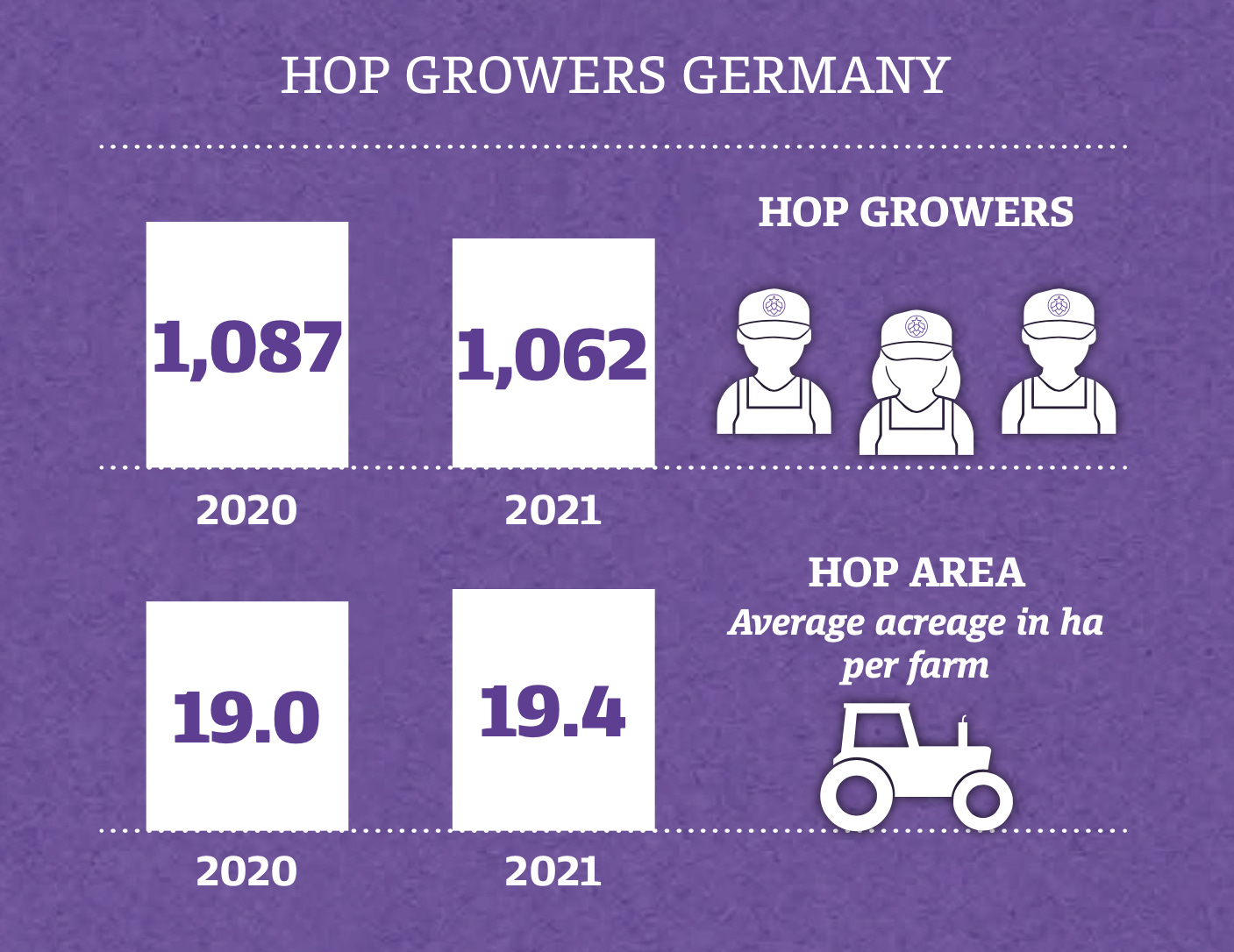

German hop farms are quite different[3]. According to the 2021/2022 BarthHaas Report, there were over 1,000 farmers there and on average those farms 18 times smaller than the average farm in the U.S. Pacific Northwest (Figure 2)[4]. The largest German hop farms are between 200-300 acres. Most are much much smaller. They, like their American counterparts, hire additional labor to help with spring work and harvest. Other than that it's a family affair with opa and oma helping out when necessary. In short, considering the outcome where the U.S. produced XX percent and Germany YY % of the 2021 crop, the two industries could not be more different.

Figure 2: BarthHaas Estimated Number of Hop Growers in Germany

Source: 2021/2022 BarthHaas Report

It's easy to understand why hop contracts have been used. They have the potential to create the perception of stability, and they give producers some idea of the demand for their product. Those are two very important things when the product produced has an inelastic demand and only one customer demographic, brewers. It's easy to imagine why a German farmer who has to wait two or three years to produce his first crop would want the stability a contract offered. It's also easy to see why an American farmer who cannot exist without bank financing wants those contracts as well. That all makes sense. Hop farms worldwide require trellis and other expensive things.

Why so far Forward?

I don't know that there's any good justification for one contract length over another. Why three years, or five years? Why not 10-year contracts? It all seems fairly random to me, and I've been in the industry for over 20 years. I can only imagine the confusion of somebody new to the industry. The case for stability and some sort of means by which to acquire is clear. That, however, is not normally the way forward contracts are used.

According to Investopedia, forward contracts in commodities are typically used by a party to hedge against anticipated price changes that would be unfavorable to them[5]. That seems like a reasonable way for a brewery with a predictable demand to lock in variable costs for the future to take advantage of favorable macroeconomic trends when they exist. That might not have been a bad idea a couple years ago given the current macroeconomic situation. Based on my experience, most brewers don't seem to buy their hops this way, but it's not by any fault of their own. It's because hop contracts are not offered in this way.

Big brewers diversify their alpha supply by sourcing from multiple countries and even multiple merchants. Proprietary varieties, which have been leveraged to create a competitive advantage for their owners' companies, makes that complicated for anybody relying upon them to do. That's by design and is partly the reason why most craft brewers don't consider diversifying their supply portfolio.

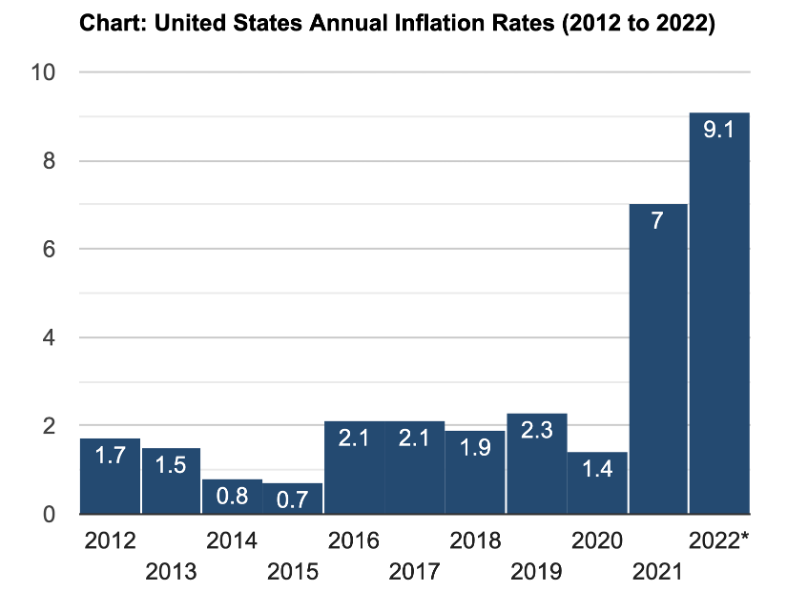

Using forward contracts in the traditional way would have made sense in recent years as hedging would have protected brewers against the recent and sudden increase of U.S. inflation numbers at 9.1% (Figure 3)[6]. Hop forward contracts, however, are not used this way. Their advertised use is not even related to hedging. Hop contracts are reactive instruments. They are not proactive even though they deal only with future production. For that reason, now that inflation has increased, brewers can expect hop prices to increase for the foreseeable future. None of the current inflation increases were priced into the hop prices brewers are currently enjoying.

Figure 3: U.S. Annual Consumer Price Index Rate of Inflation 2012-2020

Source: https://www.usinflationcalculator.com/inflation/current-inflation-rates/

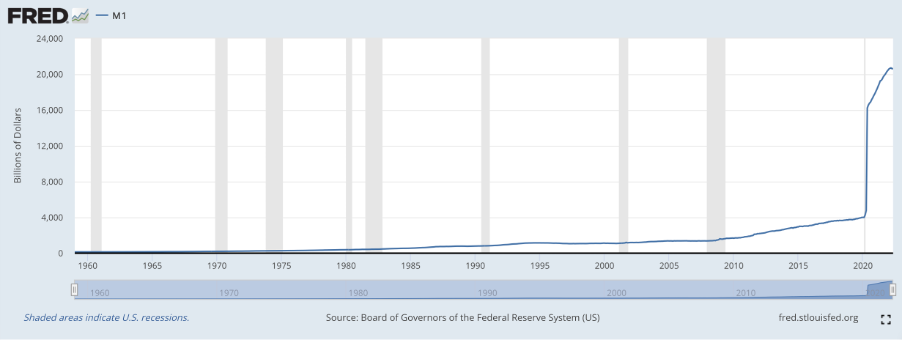

A Brief Tangent on M1

A brief tangent on inflation here because a lot of people I know haven't heard of the M1 money supply. I think it's important that people understand the scale of our current situation. During the past 15 years, there has been a disproportionate creation of U.S. Dollars by the Federal Reserve. It began in 2008 but then shifted into ludicrous mode in 2020 in response to COVID (Figure 4)[7]. That's all I'll mention about that since this isn't a macroeconomics course.

Figure 4: The St. Louis Federal Reserve Measurement of the M1* money supply.

Source: St. Louis Federal Reserve

*For an explanation of what the M1 money supply is, you can visit the Federal Reserve's web site by clicking here.

And Now, Back to our Program

Season average prices, as reported by Hop Growers of America in the 2021 Statistical Packet[8], demonstrated that average prices actually decreased in 2021 relative to 2020 (Figure 5). That is because forward hop contracts prices are related to the perceived market situation at the time of their signing, not the actual situation in the year when they come to fruition. For example, if it's a seller's market, prices for all five years of a five-year contract will be high despite the fact that every Washington and Idaho farmer knows that next year they could plant enough acres to cover any potential shortfall. That's not the point of the forward hop contract. One key feature of the forward hop contract is to extract maximum revenue from seller's markets. Supply is balanced another way.

Figure 5:

U.S. Season Average Prices and Total Crop Value 2011-2021

Source: Hop Growers of America web site[9].

Why

Jim Glassman, Head Economist of Commercial Banking at JP Morgan tells us that commodities typically act as a leading indicator of inflation?[10] Why would hop prices decrease? As a recovering hop merchant, I believe I have a pretty good idea why that is. I believe there are at least two reasons for this. I've mentioned one of them already, but I'll go into them in a bit more detail here.

Reason #1:

Hop prices are not sophisticated calculations taking macroeconomic trends into consideration like commodities traded on the Chicago Board of Trade. Forward hop contracts are instruments of fear and opportunity written privately between two parties[11] the details of which are known only to the parties involved.

The strength of the current seller's market is obvious in the most recent data regarding U.S. forward contract rates from 2022 through 2025 (Figure 1). During a strong buyer's market, such as during the period between 2001 through 2005, breweries contracted fewer hops (Figure 6). Instead, they opted for freedom and flexibility over fixed supply contracts that lockdown their purchase decisions. They could get lower prices on the spot market due to the surplus and chose to do so. Perhaps unbeknownst to them though at the time their supply was coming from old inventory in the surplus as annual production was lower than annual demand, which led to an inevitable price spike to bring things back to order in 2007 (Figure 7). Proprietary varieties have changed the way the market works. We'll talk a LOT more about that in future articles.

Figure 6: 2001 Barth Report Estimate of Forward Contract Rates 2001-2005

Source: 2000-2001 Barth Report (German edition)

Figure 7: U.S. Production & Season Average Price 1948-2021 Adjusted for Inflation

Source: USDA NASS, U.S. Bureau of Labor Statistic

* The average inflation-adjusted season average price during this period was $4.00 per pound

American hop farmers are fiercely independent. In a free market, when they're not controlled ... as they are in 2022, they're their own worst enemy. The history of the hop market is awash with examples of supply swings that brought about by boom-and-bust cycles (Figure 8). I suspect, if we had access to the data, forward contracting rates would show similarly cyclical patterns.

Figure 8: German hop prices between the years 1798-1847

Source: German hop museum in Wolnzach, Germany. One of several such images on display.

Forward contracts, therefore, are essentially a threat where the supplier says, implies or infers, "Sign this contract or you won't get my hops!". That threat only works in a seller's market. Oldtimers in the hop industry, of which I am apparently one now, remember when saying something like that would have been laughable. In today's seller's market, it's the law of the land. Of course, a buyer is free to not sign a contract. The seller can sleep easy knowing they didn't extort a contract from their customer. That's what I told myself when I was a merchant. From conversations I've had with hop merchants and farmers, it seems that's what they tell themselves too. Forward hop contracts exist to move the supply of hops and to give farmers some indication of how many hops they might be able to move in the future.

But why a three-to-five-year contract? Why not two-year contracts? Why not a contract for the current year? There might be a good reason for that. We'll get to that in a minute.

Reason #2

Hop contracts don't price in future anticipated market changes. The existing narrative regarding the cost of hop production does require it. It's hidden in plain sight. Hop Growers of America even refers to it as a "budget narrative" on the link on their web page[12]. That narrative, I believe, is a façade created by the very people who can benefit the most from inflated cost of production numbers and the increasing prices they justify, the farmers. I've written about that in the past, but the release of the new 2020 data since my previous article warrants a fresh look. That will be in an article coming soon.

In a nutshell, the WSU Cost of Production report data is voluntarily provided by members of the Hop Growers of America board. Who sits on that board? Yep ... farmers. So, we are supposed to believe the same individuals who profit from selling hops are completely unbiased. We should assume they report accurate and realistic figures that can later be used as justification for price increases. The appearance of neutrality and objectivity is generated by laundering that data through WSU. This is not to criticize the people producing the report. I am sure their methods are excellent. The report seems thorough and is very well prepared, but as the old saying goes, "Garbage In Garbage Out". This reminds me of studies funded by pharmaceutical companies whose results are biased in favor of the companies funding them. In such cases, the National Institute of Health (NIH) recommends either a firewall between the funding source and the researcher, or a separate funding source[13]. No such system has even been discussed in the hop industry. That would mean an independent audit of the actual costs of production. That's unlikely.

The WSU cost of production study combined with USDA season average price and total crop value mentioned created a situation where between 1999[14] and 2021[15] the cost of production for hops increased by 229.96%. According to those figures, the industry LOST $470.9 MILLION during that time.

If, on the other hand, we use U.S. CPI data between 1999 and 2021[16], we find only a 51.4% increase in the cost of things during that same time. Using these data, the U.S. hop industry made a PROFIT of $1.678 BILLION during that same period ... That's BILLION ... with a B! OK ... I'll admit that CPI calculations are probably not the best means by which to measure the increase in the cost of production of hops. There are other ways that would be more accurate, but they are unavailable[17].

The truth, however, likely lies somewhere in the TWO BILLION DOLLAR difference between the two estimates. You don't have to have a Ph.D. in economics to understand that if the industry lost half a billion dollars over a decade farmers would probably not have chosen to double acreage. Something smells fishy! That though is the myth the data reported by the WSU cost of production study would have you believe. Whatever the number is, keep in mind that the profit (or loss) is divided between a very small group of families in the industry (Figure 9). Follow the money.

Figure 9: BarthHaas Estimated Number of Hop Growers in the Pacific Northwest of the U.S.

Source: 2021/2022 BarthHaas Report[18]

The relationship between cost, price and contracts

In my short 20+ years in the hop industry, I've learned that the price of hops is not related to the cost of production. In other words, it has never operates on a cost-plus model. The price of hops represents whatever the market will bear. Whether that is above or below the cost of production depends on who controls the market, buyers or sellers. That is the battlefield. Low prices don't stop a hop farmer from producing hops. The same is true for contracts. Remember ... The raison d'être of a hop farmer is to produce hops. In tough times, hop farmers will continue to produce hops regardless of price or contracts. They will produce fewer of them, but they won't stop until they have no other choice.

"No one is more hated than he who speaks the truth."

- Plato

A looming threat?

The doubling of hop acreage over the past decade will be a future liability for the farmers who do not own proprietary varieties but who have expanded their acreage to grow them. They will be at the mercy of the market leaders based on the new market share discussed in the previous article, "Has a Cartel Taken over the Hop World". The decrease in acreage quantified in the article before that about the June hop acreage strung for harvest report demonstrates the degree of control present in the industry today. Brewers looking for increased efficiency will inevitably follow the direction of the macro brewers who went before them that they claim to despise. That means less wasteful uses of hops, more extracts and downstream products. Fewer acres of hops will be needed. When that happens, it will bring new challenges to the industry.

After a decade of investment and equity-building, American hop farms are well capitalized. They've invested hundreds of millions of dollars in infrastructure during that time. Again, how could they do that if they have lost half a billion dollars during that time? If the future is anything like the past, none of them will want to downsize. Egos have grown together with farm size. Any future fight for market share will be fierce. It's not hard to imagine how that will play out even despite the existence of proprietary varieties. It's a future that will bring an opportunity for the market to swing back into buyer control. This is a future that hop farmers will try desperately to prevent through the careful management of supply. Once you've sat in first class, it's hard to move back to economy.

So ... What's the Con in Contracts?

I mentioned it briefly already. Farmers say they won't sell hops without a contract. That's not true. The largest hop merchant companies, or their owners, produce large quantities of hops. They're farmers. As such, they have farmer biases. Farmers demand contracts in a seller's market (i.e., when they can get away with it). So, the con is to use the seller's market to exploit their advantageous position, leverage the effects of a short market in year n when nobody has extra hops forward to year n+1, n+2 ... n+5 when they do by getting long-term forward contracts. The goal in previous short markets has been to build equity, reinvest in infrastructure and prepare for future downward pressure on prices. Contracts are part of the way farmers say they do that. I don't doubt that entirely ... but I wouldn't believe them entirely either.

Another con

Another con about hop contracts is what makes them so attractive to suppliers. A recurring business model is more predictable, more profitable and enables more growth[19]. Think of a hop contract like a subscription to a supplier. From the supplier's point of view, it's easier to keep an existing customer happy than to convert new customers each year. With a contract, the buyer and seller are tied together. That gives the seller the advantage. Sometimes a brewery's actual needs don't match what they projected their needs were going to be. When the buyer is so large, they simply demand the contracts be renegotiated or abandoned due to their position in an oligopsony. When they are small, some understand that the cost to pursue them in court costs more than the contract is worth. Less scrupulous brewers will exploit this advantage. Unfortunately, I've had both happen to me as a merchant when market prices decreased. The incentive for farmers who own the companies that own the proprietary varieties is to manage the acreage of their proprietary varieties to maintain the perception of scarcity so the merchant companies they also own will not suffer from this fate. As soon as the perception of scarcity vanishes, prices decrease. When that happens, the current paradigm collapses. Each proprietary variety represents a legal monopoly due to their patents, enable their owners (which are companies involved in farming hops one way or another) to manage the acreage on which those hops are produced. If you can manage supply, which is driven by panic, fear and emotion[20], by the laws of supply and demand you can influence the price.

Three Alternatives to Forward Contracts:

Back when macros dominated the market, contracts made much more sense for breweries. Macrobrewers have more predictable needs. They contracted for decreasing percentages of their needs for each forward year (i.e., year n 80%, year n+1 60% ...). As each new year approached, they topped up their hop needs. There was always sufficient supply of hops or hop products ... even in 2007 and 2008 because surplus is built into the contract model. Today, large craft brewers are nearly indistinguishable from macros. Their flagship beers enjoy global reach, and they too can foresee their hop needs. They represent only a small fraction of the total number of brewers.

Most craft brewers have less predictable needs. They can't always project what they may need for beers outside of their flagship brews. Contracts are not a good fit for the craft beer model. Craft brewers have been forced into them anyway. I had to force many craft brewers to sign three-to-five-year contracts because I was forced to by farmers. "Forced" may be the wrong word. Like I mentioned above, I could have refused to sign, but I would have been denied the hops. Why? Because since 2010 the perception of short supply has prevailed. That puts farmers in control of the market. That's all it takes to make forward contracts obligatory.

The smallest 7,500 - 8,500 craft brewers in the U.S., try to compete for market share in an increasingly competitive market. It's difficult for them to know what they'll need next year due to changing tastes. The following three alternatives are strategies I would try if I was responsible for purchasing hops at a brewery.

Alternative 1

I would buy more public varieties and rely less on proprietary varieties. I would buy them directly from farmers if possible. If that's not possible, I would try to be as direct as possible. The more people involved between A and B; the more money brewers leave on the table. There are local independent hop merchants in every hop producing country. There are schiesters in the hop world though, so I'd be careful, but it's a small world.

I wouldn't do this alone unless I was working at a medium-sized brewery that used thousands of pounds of hops. I'd join with other breweries to make my order larger. The larger the better. Even if I worked at a medium sized brewery, I'd look for somebody to partner up with. It's inconvenient for hop farmers to sell 50 pounds or 50 kilos of hops. It's also expensive to ship those whether it’s around the world or across a state. Expensive shipping doesn't sound like a good reason to trade away freedom. If I could build an order that required thousands of pounds of raw hops or pellets, it would pique the interest of any farmer or any independent merchant. They'll want to work with me. Most PNW farmers can arrange for the pelleting. I'd suggest the terms mentioned in Alternative 3 or some variation of them. Nobody is offering anything like that. If I did something different like that, I'd stand out from the crowd that is content to go with the status quo.

Why would I choose public varieties? Because nobody can legally control the acreage or influence the price of public varieties. Farmers are free to plant as many of them as they want. They can sell them for whatever price sounds good to them. That's not the case with proprietary varieties. Some public varieties compete for the harvest window with popular proprietary varieties though. I wouldn't expect this to be a cheap and easy strategy that falls in my lap. It would take work.

Alternative 2

I would use generic alpha (not variety specific) in extract form. According to the 2021/2022 BarthHaas Report, there was an estimated surplus of alpha acid in the world in 2021 of 2,347 metric tons (5.17 million pounds) of alpha acid[21]. Since alpha is a homogenous product that enjoys commodity pricing, I know I could get a better deal than I would by buying the most popular brand name proprietary varieties. I'd shop around. German hop farmers have sold their alpha hops at prices American farmers would not even consider. There are huge opportunities for savings. If the brewery I worked for had skilled brewers, I would understand they could use whatever hop offers the flavors they needed in a dry hopping situation.

I'm not a brewer, and I don't play one on TV. I've spoken with more brewers over the years than I can count though. I've been told changes like the ones I mentioned above are something a skilled brewer should be able to figure out with a little work and experimentation. I would combine the joint order strategy from Alternative 1 with payment in full at the time of purchase and I'd buy on the spot market to get the best prices. I bet I could save 50% on my hop bill by doing that.

Both alternatives 1 and 2 will be liberating. They offer brewers the opportunity to source product directly from a farmer, or from a merchant who is independent of the structure that dominates the industry today.

Alternative 3

How much is the security of a forward contract worth? I asked a hop farmer not too long ago if he would grow hops on a year-to-year basis without a contract. I asked if different payment terms would enable him to produce hops without a contract. Specifically, I asked him how much more money would he need to do that. His answer might surprise you.

Here's one hypothetical payment schedule I suggested:

The months and payments are for hops produced and purchased in one year without a contract.

April: 30% of the total payment

May: 10% of the total payment

June: 10% of the total payment

July: 10% of the total payment

August: 10% of the total payment

September: The final 30% of the total payment

Here's another hypothetical payment schedule I suggested:

I also suggested a schedule of 12 equal monthly payments beginning after the harvest of the previous year, so the final payment coincides with harvest of the year my hops are ready.

The farmer I spoke with told me that either of those systems would work for him if anybody would offer. I asked him with that payment schedule without contracts how much of a premium he needed to compensate him for the perceived lack of stability. His answer was that he's probably add, "an extra 10-15% per pound and that would probably be enough."Those numbers could change depending on the farmer in question. Of course, anecdotal evidence that the system can change. I mention that only to demonstrate that contracts are not the only method to offer stability to a farmer.

This strategy would:

Change hop sales to a merit-based system rather than locking buyer and seller together based on fear and opportunity.

Increase the incentives to deliver high quality hops and service to customers.

Encourage farmers to compete based on their perception of the risk associated with spot sales. In other words, farmers with a high confidence in their ability to produce a high-quality crop could negotiate that percentage down closer to parity with forward contracts.

Encourage realistic contracting levels for the current year based on actual needs.

Return freedom to brewers with changing needs.

Eliminate huge lump sum hop payments to fit better with cash flow

Remove, or significantly reduce, the need for the farmer to borrow money from the bank lowering production costs.

Facilitate prices that more adequately reflect the supply and demand situation given macroeconomic conditions.

Create an opportunity for those willing to contract to still get a slightly lower price, at the cost of their freedom.

Reality Check

There's nothing wrong with any of the alternatives mentioned above. I doubt brewers will be proactive and change the current system. That would be a time-consuming difficult thing in a world where most people are so busy, they take the easy route just to get everything done. It's like the person who doesn't check every so often to see if they can save money on their mobile phone bill. Usually you can save money ... especially if the provider thinks they might lose a customer. Hops are no different. That's one reason why brewers leave money on the table when they buy hops. I'll share more in future articles. In the meantime, suppliers and farmers profiting from the status quo won't suggest anything remotely even resembling any of these strategies. They don't need to. They're making tons of money already.

Macro brewers and large craft brewers have the power to demand this and other changes if they prefer freedom to contracts. Their size gives them special status. They can negotiate special deals not available to the public, much like Warren Buffet did after the 2008 mortgage crisis[22]. Macros and big craft breweries are treated differently than small breweries. Smaller craft breweries, however, are the ones who would benefit the most from a change in the way hops are sold. To gain an advantage, they must unite.

Despite claims to the contrary, a single small brewery's business is smaller and therefore less significant in a money driven industry. As I've heard so many times over the years, "It takes as much work to sell 100 pounds of hops as it does to sell a container." That's how merchants think about brewery deals, from a processing point of view. So long as it is a seller's market, the small brewer's needs are secondary. I know because I've had those types of conversations with other merchants. This, I believe, is the main reason for the larger merchant groups to cooperate with channel partners enabling the segregation of customers by size. Smaller customers are handed off to channel partners who can invest more time servicing their needs ... and charge more for their service.

If a group of smaller brewers cooperated and consolidated purchasing power, they could enact the change they need with the right leader. This is a dangerous proposition. The handful of people with the greatest influence in the hop industry own companies with tentacles that reach around the globe influencing many other players ... not unlike John D. Rockefeller’s Standard Oil company of the early 20th century pictured above[23]. Resistance is possible. It is necessary. Based on their behavior, it seems the goals of the people in charge of the hop industry today are interested in nothing less than total control. If they are left unchecked, in a few short years, under the status quo, they may just get it all.

Conclusion - Irony and Travesty

Buying a disproportionate quantity of proprietary varieties as the craft brewing industry has done over the past decade has consequences. Its effects have already been seen. Ultimately, if brewers are content with ever higher sustainable hop prices increasing at over four times the rate of inflation, they should continue the status quo. If they believe they are getting so much value from proprietary hops that they are willing to trade their freedom and fortune for it, then perhaps full spectrum dominance of the hop industry by a handful of men is the best outcome.

The ultimate irony is that craft brewers who themselves represent independence, artisanal craftsmanship, art, passion, local production and so many other ideals people want to believe in have empowered global corporations. Their actions have led to monopoly control of monocrops that produce tens of millions of pounds of privately-owned hop varieties each year. This dichotomy should not be lost on anybody. That the word sustainable is used in the process is a travesty.

Continuing the status quo will bring greater consolidation of power in the hop industry. Proprietary varieties in the U.S. today account for "only" 70-75%. It can get worse. If that happens, there won't be many independent farmers. There will be even fewer independent merchants. That won't happen by accident.

These articles are free. If, however, you found some value in what you read and would like to provide some value in return, you can donate here. There’s no obligation to donate if you cannot afford it.

I would like to thank everybody who took the time to read this and other articles I've written. The level of support from people all over the world tells me there were many people craving this type of information. I will do my best to continue to prepare articles that bring you value.

I sincerely hope you found this article interesting. If you haven't already, I hope you will consider subscribing. I'll be publishing something around the 1st and 15th of each month so as not to fill up your inbox.

[1]https://www.barthhaas.com/fileadmin/user_upload/kampagnen/barthhaas_bericht/2022/BarthHaas_Report_2021_2022_EN.pdf

[2] USDA NASS NHR 2012-2021

[3] I will highlight Germany in this case because Germany and the U.S. produce similar quantities of hops, approximately 40% of the world market each. No other hop producing country produces anywhere near as much, but the infrastructure of many European hop producing countries resembles that of Germany's.

[4]https://www.barthhaas.com/fileadmin/user_upload/kampagnen/barthhaas_bericht/2022/BarthHaas_Report_2021_2022_EN.pdf

[5] https://www.investopedia.com/terms/f/forwardcontract.asp

[6] https://www.usinflationcalculator.com/inflation/current-inflation-rates/

[7] https://fred.stlouisfed.org/series/M1SL

[8] https://www.usahops.org/img/blog_pdf/405.pdf

[9] https://www.usahops.org/img/blog_pdf/405.pdf

[10] https://www.jpmorgan.com/commercial-banking/insights/commodities-inflation-and-whats-ahead-for-businesses

[11] This is referred to as an Over the Counter (OTC) trade

[12] https://www.usahops.org/growers/cost-of-production.html

[13] https://pubmed.ncbi.nlm.nih.gov/23135338/

[14] This data is no longer publicly available. Fortunately, I have a copy and will make that available to subscribers of the MacKinnon Report when I write the updated article on the cost of production. For now, I can tell you the total cost of production in 1999 was $4,118.28 per acre

[15]https://www.usahops.org/cabinet/data/TB38E%20Conventional%20and%20Organic%20Hops%20Enterprise%20Budget%20in%20PNW.pdf

[16] https://www.usinflationcalculator.com/inflation/consumer-price-index-and-annual-percent-changes-from-1913-to-2008/

[17] The Consumer Price Index (CPI) is not the most appropriate measure of inflation for hop farmers because it includes sales tax and other costs on consumer related products that do not pertain to farmers but does not include fuel costs, which began to increase in 2021. A Producer Price Index (PPI) that considered all the relevant costs would be more appropriate, but no such index exists. The net result of using CPI is likely a higher rate of inflation than with an available PPI from another industry. Ultimately, this means that estimates of potential profits for the industry during that time might be understated, but we really don't know.

[18]https://www.barthhaas.com/fileadmin/user_upload/kampagnen/barthhaas_bericht/2022/BarthHaas_Report_2021_2022_EN.pdf

[19] https://www.forbes.com/sites/forbestechcouncil/2020/10/26/how-a-subscription-business-can-increase-business-valuation/?sh=330ed204b2e7

[20] https://www.nasdaq.com/articles/the-law-of-supply-demand-2020-04-21

[21]https://www.barthhaas.com/fileadmin/user_upload/kampagnen/barthhaas_bericht/2022/BarthHaas_Report_2021_2022_EN.pdf

[22] https://www.businessinsider.com/warren-buffetts-8-most-profitable-deals-ever-2017-11?op=1#1-a-bet-on-brains-that-paid-off-1

[23] Accessed online at: https://profesorjuliodapenalosada.blogspot.com/2013_01_01_archive.html