Propaganda, half-truths and fear porn

... and how they're used to increase prices and get brewers to sign contracts

CONTRACTING IN A SURPLUS

Since my last article, so many readers shared their experiences with me[1]. Thank you! Some shared that their hop merchants are urging them to contract for 2024 and 2025 now. They said this year’s acreage reductions will mean the varieties they want will be in short supply. This is the type of half-truth fear porn brewers might hear from people trying to sell them hops. They shouldn’t fall for that trick.

Should any brewer contract for those proprietary varieties in 2023? I documented how there are at least 54 million pounds of surplus proprietary hop varieties in 2023 in an earlier article of mine called “Hop Inventory Facts You Didn’t Know”[2]. If we assume those hops have been stored under proper conditions, they won’t lose significant brewing value for several years[3]. This month, I’ve spoken with brewers who do not need the 2020, 2021 and 2022 hops they contracted. It seems there are massive quantities of contracted 2023, 2024 and 2025 hops that are also not needed. A brewer today can find millions of pounds (hundreds of metric tons) of popular varieties.

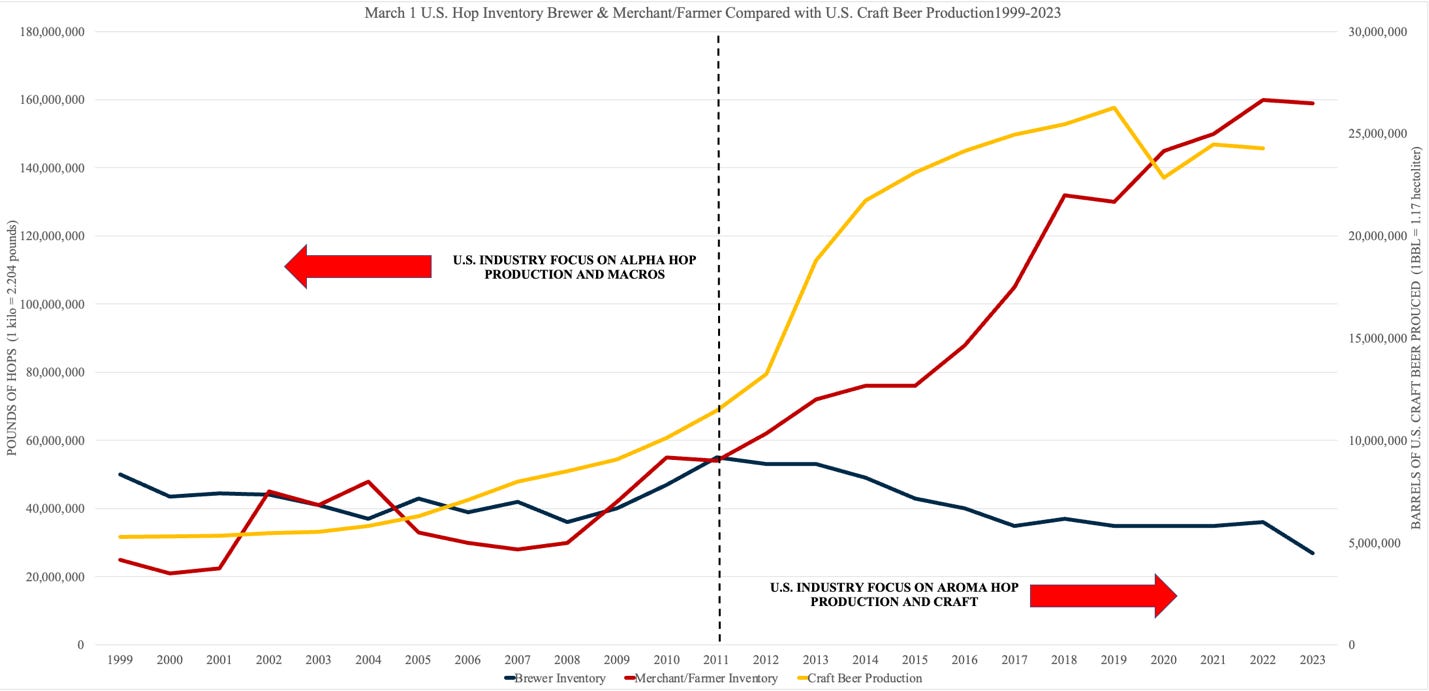

This is a good opportunity for brewers to revisit three of the graphs from the article I mentioned above. They demonstrated how inventory has increased along with increasing proprietary variety dominance (Figure 1). They show the increasing disparity of inventory between merchant/farmer and brewers (Figure 2). They show the high levels of forward contracting rates during the previous decade (Figure 3).

Figure 1. USDA March 1 Hop Stocks Data 1970-2023

Source: USDA NASS 2023 March 1 Hop Stocks Report 1970-2023

Figure 2. USDA March 1 Hop Stocks Data 1999-2023 vs. Craft Production

Source: USDA NASS 2023 March 1 Hop Stocks Report 1999-2023, Brewers Association

Figure 3. IHGC Sold Ahead Data 2012-2022

Source: IHGC Country Reports 2012-2022

The divergence of inventory held by brewers and that held by merchant/farmers is an order of magnitude greater than any time during the last half century (Figure 1). Merchant/farmer inventory exceeding brewer inventory is one sign of a surplus. The imbalance results from too many hops chasing too little demand (i.e., hopflation). Figure 2 demonstrates the abrupt slowdown of the craft industry since 2019. It is important to remember that the reported surplus consists of hops from all countries stored in the U.S. The slowdown of the craft industry creates a problem for the global hop industry. Figures 1 and 2 demonstrate that supply imbalances occurred in 2004 and 2010 (prior to proprietary hop dominance). There has been an imbalance every year since 2012. The two common points of failure of these three periods were the inability to forecast demand combined with strict forward hop contracts locking brewers into supply agreements.

There is nothing inherently bad about proprietary hop varieties. The problem comes from a patent system that empowers companies with monopoly control over the food we eat, or, in the case of hops, the ingredients in the beer we drink[4][5][6].

HOP SOCIALISM

The American hop industry has yearned for centralized control for decades. The 2023 hop surplus[7] is the embodiment of the most recent attempt at central control over U.S. hop sales. Previous attempts were in the form of three failed Federal marketing orders run by farmers during the 20th century. The problem with centralized decision making is that central control doesn’t overcome man’s inherent greed. That is true whether it is a Federal marketing order or a private company that owns the proprietary varieties produced on half the U.S. hop acreage. Central committees didn’t work for the Soviet Union. It is arrogant to think they can work in the hop industry.

“Never attribute to malice that which is adequately explained by stupidity.”

- Hanlon’s Razor[8]

Proprietary varieties created a monopoly that manages the production and distribution decisions for over half of U.S. hop production[9]. The increased market concentration they created has reduced competition[10]. The problem is that central control over supply doesn’t help forecast demand[11]. Brewers cannot predict the future any better than the rest of us. Forward hop contracts represent their best guesses of their future needs . The lack of accurate information leads to poor decisions on both sides of the contract[12]. The result is increased inefficiency and reduced productivity. Central planning fails because nobody can beat the genius of the market[13][14]. That is one of the challenges of the current hop market.

Acreage cuts in 2023 were a good first step toward balancing the market. That would not have been possible without the absolute monopoly power that dominates the U.S. industry today. It seems the industry is stuck at the point where merchant/farmers are insisting brewers fulfill their contracts. I can only speak from my experience and about my mistakes, but the current situation looks very familiar.

The business model U.S. merchant/farmers have enjoyed for the past decade has fallen apart. Based on the size of the problem, I expect merchant/farmers will need to compromise on existing contracts. If they are serious about restoring control over the market sooner rather than later, they will cut production by another 15,000 acres (6,072 hectares) in 2024. That will create a hole big enough for surplus hops to move into the market during 2024, 2025 and 2026. I anticipate merchant/farmers will apply pressure to brewers to get them to fulfill contracts and/or sign new contracts. It would be good for brewers to be aware of some of the tactics that will be used against them.

PROPAGANDA (a.k.a. Marketing)

Everybody knows somebody who buys the latest iPhone every year. This happens in the hop industry too. There are brewers who believe they have to have the latest crop. They do that for several reasons:

1) There’s perceived scarcity[15] (I discussed this as it relates to hops in my previous article, “Mafia Tactics Used in the Hop Industry”)

2) the phone has become part of their image (I discussed this as it relates to hops in my previous article, “Who Owns Your Beer”)

3) some people just feel they must have the latest and greatest edition of their phone. (This is like the false belief by brewers that the current crop is the best and they must have it to get the best hops.)

Apple trained people through well thought out marketing campaigns to behave in a way that is profitable for Apple[16]. Prices have a counterintuitive influence on people. Higher prices lead people to believe they are getting something of real value[17]. It’s easy to sell hops and get brewers to sign contracts when prices are high than when they are low. That does not mean the brewer is getting what he’s paying for. Google and other tech companies manufacture scarcity around their products and services to use scarcity as a marketing strategy[18]. When Gmail began, some of you may remember you needed an invitation to open an account. Access to those invitations expired to create a sense of urgency[19]. Some of the companies marketing proprietary hop varieties appear to have sophisticated market strategies designed to do the same. (Think: You won’t be able to get those hops without a contract.)

In a recent Johns Hopkins University study, scarcity, or even the perception of scarcity, changes the purchasing behavior of consumers. People buy more of the thing they believe to be scarce. Scarcity bias causes people to rate the quality of scarce products higher than less scarce products[20][21]. This is referred to as the scarcity principle[22]. This applies to hops. Acreage of the “scarcest” varieties over the past five years has increased to the point where they are among the most widely planted in the U.S. (Figure 4). Combined with surplus stocks data (Figure 1), it’s difficult to make a case that scarcity ever existed. It seems the brewing industry was played.

Figure 4. Ten Most Widely Planted U.S. Varieties in the Pacific Northwest 2017-2022.

Source: 2022 Hop Growers of America Statistical Report[23].

SIDE NOTE:

I attended the most recent Craft Brewers Conference in Nashville, Tennessee. It was great to see a lot of friendly faces. There were quite a few people, however, whose faces revealed they were not so happy to see me. Awkward smiles and reluctant handshakes came mainly from people involved in the U.S. hop industry. More than one person suggested I was brave to be walking around the trade show, or that I should watch for knives coming my direction. Those were good for a laugh. A brewer said I’m “ballsy” for even writing about these things. After the show, I was thinking how interesting it is that these articles are controversial at all. I am just assembling documented facts about the industry and with the benefit of over two decades of experience in the industry providing some analysis. I cite my sources and mention when something is my opinion so as not to mislead anybody. I leave out so much because there are no public sources that confirm the things I could share. If I were a brewer, I would be curious why these articles are the only source for this type of information. The things I write about are common knowledge among insiders in the hop industry. If I were a brewer, I would wonder why the people who sell me my hops are not happy that some guy is writing about these things.

HALF TRUTHS

Every merchant knows that farmers like to complain about the risks they face while producing the crop. The joke among merchants used to be that farmers will lose their crop 10 times before each harvest. Then, magically, they produce an average crop. I’ve seen this more times than I can remember. Today, the line between merchants and farmers is more blurred than ever, which is why I refer to them as merchant/farmers. Complaints about production problems once reserved for merchants with the context necessary to interpret them now reach brewers around the world via social media and email who lack the proper context.

Below, I’ve listed a sampling of some of the more common potential threats to the crop brewers might hear.

1) Numbers out of context. Lack of context in a report can be confusing, which makes the information difficult to interpret. The following excerpt from a 2021 hop report is an example. “On June 24th a hailstorm ran across parts of the Saaz growing region. A region of approx. 500 ha (1,250 acres) was damaged to varying degrees, in some cases severely (20 – 100%)”[24]. This may be valuable information. Without knowing the total size of the growing region, the varieties in it and a better estimate of the anticipated damage, it is useful to create the impression of an impending shortage. FOLLOWUP: According to the International Hop Growers Convention, the Czech Republic produced 8,400 MT in 2021, a 41% increase over the 5,925 MT produced in 2020[25]. It seems that hailstorm didn’t cause too much damage. Hops can recover from early hailstorms. If a hailstorm hits later in the year, it can be devastating. The brewer doesn’t know that. To a brewer without the proper context hailstorm = bad.

2) Early crop problems. “We’re off to a slow start”, or “The crop is two weeks late”. “The spring has been too cold and wet.” These are all variations on the same theme, the year has already begun … and we’re in trouble already. In 2017, this article in the Seattle Times documented the slow start that year. In 2017, Yakima enjoyed 71 days with temperatures higher than 90 degrees Fahrenheit, the most since 1892[26]. A slow start in the early part of the year can be fixed with a week of heat at the right time. In general, brewers don’t need to be concerned with early slow starts. That’s a farmer issue. Brewers don’t know that though. FOLLOWUP: According to the USDA, the 2017 crop returned the second highest yield between 2017 and 2022[27]. That early slow start does not seem to have affected the crop.

3) Too much of X. “The fields are too wet.” or “…rainfall was insufficient from April to June” or “We can’t get in to train/spray/plant (insert verb of choice here)”. According to the 2016/2017 Barth Report this is exactly what happened in Poland in 2016. The Barth report is exceptional. Since it is prepared once a year, its authors have the benefit of hindsight. They do a great job presenting the entire year in summary. The reader can see that the wet spring and the lack of rain did not affect average yields, which increased from 1.72 MT/ha to 2.29 MT/ha.

4) Disease and pests. “Created a lot of downy and powdery mildew pressure.” Or “It’s been a bad year for downy mildew” (usually from high humidity). A crop report like this 2022 report from Yakima Chief Hops™ (YCH) can scare brewers early in the year[28]. Powdery mildew is something to be concerned about, but farmers have plenty of experience fighting it. They know which pesticides will reduce the threat and they have plenty to choose from[29]. To be fair, the YCH report stated that after things heated up it would eliminate that pressure and that farmers expected an average crop[30]. A good report puts the threat in perspective for the reader. That doesn’t always happen. According to USDA National Hop Report, hop yields in 2022 were the lowest this century[31].

5) That could cause a shortage. “We didn’t get enough snow over the winter.” Or “We’re not sure if there will be enough water this year.” This CNBC article documents how the lack of snowfall, and “adequate water” would create potential shortages in 2015. Hop Growers of America reported in their 2016 Statistical Report that the U.S. produced 80.3 million pounds of hops (36,423MT) in 2015, an increase of nine million pounds (4,082MT) over 2014 U.S. production[32]. Prior to 2015, the U.S. had only produced such a large crop twice before, in 2008 and 2009[33].

If you have found some value in this article, I would like to ask you to share it with somebody who might also find it valuable. I don’t think you’ll find these topics or the valuable insight provided in these articles anywhere else. They are free because it is not available anywhere else, but it is information I believe everybody should know.

I enjoy writing these articles. If you are received this from a friend and are reading it for the first time, please consider subscribing today. It costs nothing and you’ll have access to other information I plan to make available in the future.

FEAR PORN

Of course, fear porn extends beyond the five threats listed above. The winter can be too warm. Spring can heat up too fast. Summer can be too hot. It can be too cold. There can be hailstorms. The crop can mature too quickly. Hop cones can be lighter than normal. The list of the different diseases for hops alone is overwhelming[34].

All those things and many more can affect hop yields. That’s why fear porn works so well. The fear comes from a legitimate source. Merchant/farmers in the U.S. have decades of experience and an army of consultants that enable them to overcome all but the most difficult challenges. The ability of hop farmers to produce an average crop in the face of almost any challenge is impressive! Brewers don’t understand that part of the equation. The trick is to emphasize the negative while downplaying the positive. Mentioning potential threats creates the fear of a short crop. Without years of experience in the hop industry, brewers might assume the worst. Fear of a short crop increases the chances brewers will sign contracts. You will never hear a merchant/farmer forecasting record yields. Don’t forget, about half the time yields are above average. Brewers might hear that news and think that there is no reason to hurry to sign contracts. The hop business is all about getting brewers to sign contracts.

BONUS:

An amusing thing to watch for: When problems with the crop are discussed in detail, the person talking about them will point out the problems with somebody else’s varieties, or perhaps a different growing region altogether, never their own. Information regarding the quality of their crop will always be presented in a positive light[35]. Brewers lack the necessary filters to catch these and other subtleties, which make the report look objective.

FORWARD CONTRACTING IN 2023?

Contracts are advertised as a way for brewers and merchant/farmers to be partners. Merchant/farmers say some variation of the following: contracts …ensure you can secure the varieties and volumes you need at a fixed price and from a consistent crop year lot[36][37][38][39]. I’ve used that with brewers in the past. It’s another half-truth. It’s not a lie. The drawbacks of contracts for brewers are never mentioned. Contracts, the way they are currently designed, are not equitable because brewer and merchant/farmer interests are not aligned.

For example … current contracts did not anticipate inflation might make it difficult for European farmers to break even in 2023. They also cannot anticipate a hop market in decline. With a surplus of proprietary U.S. varieties looming, lower prices for one- to three-year old crop are inevitable. They will have the power to drag the premium paid for the current crop lower. Brewers who know their hops know this. They also know that properly packaged and stored pellets retain their brewing value for several years. This is an opportunity for some brewers to source their supply from surplus hops or to move away from proprietary varieties altogether.

Is it reasonable for hop merchants to demand forward contracts in 2023 at fixed prices and volumes? Consider some of the things that may happen during the life of a five-year contract signed today and how that may affect the brewing industry?

1) At the CBC in Nashville, Bart Watson said in a presentation that he anticipates zero to low growth in the craft industry going forward[40][41].

2) Gen Z is drinking 20% less than their millennial counterparts[42][43].

3) Taiwan anticipates China will invade it by 2027[44][45]. The U.S. has said that it will defend Taiwan with American troops if that happens[46]. Four-star U.S. general Mike Minihan, head of the Air Force’s Air Mobility Command, anticipates a war with China as early as 2025[47].

4) The U.S. is at risk of losing its status as the global reserve currency and having a weaker international status[48][49]. The BRICS nations (Brazil, Russia, India, China and South Africa) have agreed to sell to trade with each other without using U.S. Dollars[50]. The BRICS economies matched the G7’s contribution to the global economy in 2020[51]. By 2028, the economies of BRICS will be 27% larger than the G7[52]. Nineteen countries recently applied to join the BRICS alliance, and Saudi Arabia is interested[53][54]. In the future, there will be competition for the first time since the Bretton Woods Agreement in 1944[55]. The effects on the U.S. economy if that happens are unknown, but there are some dire predictions that would affect American’s ability to purchase luxury products like craft beer[56].

5) Population is below the replacement rate in the U.S. and EU[57][58]. The result is shrinking aging populations. The average craft beer drinker is between 21 and 44[59][60]. The potential craft market in the future will be smaller in the future.

Brewers should be cautious about entering fixed contracts with their hop suppliers now. The style of forward contracts available today do not allow for the flexibility brewers will need in the future. The brewers association should provide education about the potential pitfalls associated with hop contracts. Considering the size of the hop surplus in 2023, it is a buyer’s market. Hop farmers are in a difficult position. Their farms are twice the size they were 10 years ago. None of them want to farm fewer acres in the future than they do today. When they realize the acreage they removed in 2023 will not return, they will consider alternatives to the status quo to maintain any acreage they can. That represents an opportunity for brewers. Rather than shifting to spot contracts as brewers have done for decades, they can change the way hops are contracted. That would be a hop revolution.

[1] I’d also like to thank the people who spoke with me at the CBC in Nashville. It was wonderful to be among so many familiar faces with whom I’ve shared good memories over the years.

[2] That 54-million-pound number is a number I can demonstrate with statistics. I believe the actual surplus may be much larger than that. I have done some math based on trends and speculation that demonstrate how that number could be much closer to 100 million pounds. In these articles, I prefer to discuss well established facts whose sources I can cite from online sources that readers can check for themselves. My own opinions can be biased just as easily as anybody’s. For that reason, I will stay away from speculation, or clearly mention when a statement is based on my own thoughts and analysis so they are not mistaken for established facts.

[3] https://www.mdpi.com/2223-7747/12/4/936

[4] https://lawecommons.luc.edu/cgi/viewcontent.cgi?article=1044&context=lclr

[5] https://belonging.berkeley.edu/bowman-v-monsanto-monopoly-over-global-food-system

[6] https://issues.org/barton/

[7] https://www.hoptalk.live/post/too-many-hops-10000-acre-cut-needed-says-barth

[8] https://bpb-us-e2.wpmucdn.com/sites.uci.edu/dist/1/863/files/2021/08/Hanlons-Razor.pdf

[9] According to USDA data regarding proprietary variety production reported in the annual National Hop Reports.

[10] https://www.brookings.edu/blog/fixgov/2018/01/05/the-consequences-of-increasing-concentration-and-decreasing-competition-and-how-to-remedy-them/

[11] https://plato.stanford.edu/entries/neurath/political-economy.html

[12] https://www.elibrary.imf.org/view/journals/022/0031/004/article-A001-en.xml

[13] https://www.fraserinstitute.org/studies/abject-failure-of-central-planning-during-covid

[14] https://www.forbes.com/sites/johntamny/2022/08/07/central-planning-fails-just-as-much-when-conservatives-are-the-planners/?sh=60f94545112c

[15] https://blog.hubspot.com/marketing/the-scarcity-principle

[16] https://www.cnbc.com/2020/12/08/the-psychology-of-new-iphone-releases-apple-marketing.html

[17] https://www.choicehacking.com/2022/03/07/apples-marketing-case-study-iphone/

[18] https://www.marketingweek.com/richard-shotton-scarcity-wordle/

[19] https://groups.google.com/g/gmail-users/c/cYk6n5PR6aw

[20] https://srcd.onlinelibrary.wiley.com/doi/abs/10.1111/cdev.13368

[21] https://www.sciencedaily.com/releases/2015/02/150206145206.htm

[22] https://www.investopedia.com/terms/s/scarcity-principle.asp

[23] https://www.usahops.org/img/blog_pdf/435.pdf

[24] https://www.hopmalt.vn/hop-report-june-2021/

[25] http://www.hmelj-giz.si/ihgc/doc/2021_NOV_IHGC_ECReport_public.pdf

[26] https://www.extremeweatherwatch.com/cities/yakima/yearly-days-of-90-degrees

[27] https://www.usahops.org/img/blog_pdf/405.pdf

[28] https://apnews.com/article/55f7a460733967cf42c2dce0a561232f

[29] https://www.usahops.org/growers/plant-protection.html

[30] https://www.yakimachief.com/commercial/hop-wire/july-5-2022-field-report

[31] The source for this were data from USDA National Hop Reports from 2000-2022

[32] https://www.usahops.org/img/blog_pdf/76.pdf

[33] https://www.usahops.org/img/blog_pdf/11.pdf

[34] https://www.usahops.org/cabinet/data/4.pdf

[35] https://hopandbrewschool.com/event/harvest-update-state-of-the-industry-2-2/

[36] https://daily.sevenfifty.com/why-brewers-should-be-going-to-hop-harvests/

[37] https://www.yakimachief.com/commercial/hop-wire/cascade-centennial-contracting

[38] https://shop.barthhaasx.com/s/hop-contracts

[39] https://www.crosbyhops.com/shop-hops/hop-contracts

[40] https://www.profoodworld.com/industry/beverage/article/22861573/craft-brewers-need-to-find-new-ways-to-innovate-and-grow

[41]https://www.brewbound.com/news/bart-watson-slow-to-no-growth-crafts-new-normal-opportunities-in-new-channels-and-occasions

[42] https://www.businessinsider.com/millennials-gen-z-drag-down-beer-sales-2018-2

[43] https://www.theguardian.com/commentisfree/2022/aug/11/like-many-of-my-fellow-gen-z-getting-drunk-is-not-on-my-agenda

[44] https://news.usni.org/2021/06/23/milley-china-wants-capability-to-take-taiwan-by-2027-sees-no-near-term-intent-to-invade

[45] https://www.rand.org/blog/2021/11/taiwan-is-safe-until-at-least-2027-but-with-one-big.html

[46] https://www.reuters.com/world/biden-says-us-forces-would-defend-taiwan-event-chinese-invasion-2022-09-18/

[47] https://time.com/6251419/us-china-general-war-2025/

[48] https://markets.businessinsider.com/news/currencies/de-dollarization-renminbi-dollar-vs-yuan-takeover-china-russia-usd-2023-4

[49] https://markets.businessinsider.com/news/stocks/the-us-is-facing-a-major-challenge-as-petrodollar-loses-force-1032063614

[50] https://foreignpolicy.com/2023/04/24/brics-currency-end-dollar-dominance-united-states-russia-china/

[51] https://intellinews.com/brics-bloc-advances-another-step-as-saudi-arabia-joins-china-s-sco-275267/

[52] https://www.businesstoday.com.my/2023/04/21/brics-set-to-overtake-g7-in-global-economic-growth/

[53] https://intellinews.com/brics-bloc-advances-another-step-as-saudi-arabia-joins-china-s-sco-275267/

[54] https://www.bloomberg.com/news/articles/2023-04-24/brics-draws-membership-requests-from-19-nations-before-summit

[55] https://www.npr.org/sections/money/2019/07/30/746337868/75-years-ago-the-u-s-dollar-became-the-worlds-currency-will-that-last

[56] https://nsjonline.com/article/2022/09/what-happens-if-the-united-states-loses-its-world-reserve-currency-status/

[57] https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Fertility_statistics

[58] https://budgetmodel.wharton.upenn.edu/issues/2022/7/8/measuring-fertility-in-the-united-states

[59] https://www.brewbound.com/news/power-hour-nielsen-shares-2019-craft-beer-consumer-insights/

[60] https://www.craftbrewingbusiness.com/featured/understand-age-changing-demographics-craft-beer-drinkers-market-properly/