INTRODUCTION

Most brewers enjoyed the countless new proprietary varieties released over the past decade. Many didn’t mind paying premium prices because they were told they were supporting a farmer. Due to their lack of perspective on hop industry politics they missed that benefitting brewers was never the reason for creating proprietary hop varieties. The surplus has pulled back the curtain revealing what was really going on. There will be more new proprietary varieties if that’s what brewers want, but not because they want them. It will come at the expense of independent merchants and farmers who didn’t want to take orders from a central planning committee, and those who could have become a threat. They will be targeted for elimination. The cartel that gained control of the hop industry has the chance to tighten its grip. Monopolies stifle competition, raise prices to consumers and reduce innovation[1][2][3]. Brewers would be smart to support the survival of independent hop merchants and farmers. Competition encourages higher quality, greater selection and more innovation[4]. If you care about supporting independent farmers and merchants, there’s a simple solution.

THINGS ARE NOT WHAT THEY SEEM

The rapid growth of hop demand between 2012 and 2022 created a false sense of security among farmers and the merchants that don’t own the most popular proprietary varieties. They believed they were accepted into the inner sanctum because they were allowed to grow, sell or brew with those varieties. Some still don’t understand how they are sowing the seeds of their own demise by promoting their competitors’ varieties.

They should ask themselves the following question, “In the long-term, why does a bigger merchant company with global reach need a smaller company to help them do a job they themselves can do?”

FREE HOPS

Until 2012, hop price spikes and the production deficits that caused them were short-lived. Surpluses, on the other hand, lasted for years[5]. Spot prices are more sensitive to supply changes[6]. Double digit craft beer growth in the U.S. combined with a preference for American proprietary varieties enabled a cartel to manage supply and price. Using their power, they created the perception of a deficit that lasted over a decade. That enabled them to charge premium prices year after year, which affected the global market (Figure 1) [7].

Figure 1. Hallertau spot vs contract prices 1997-2023

Source: HopSteiner Guidelines for Hop Buying 2023[8]

Following a decade-long boom, American merchant/farmers were lulled into a false sense of security by a perpetual seller’s market. Once the growing surplus could no longer be denied, however, the merchants who helped cause it through aggressive forward contracting acknowledged its existence[9]. As the old saying goes, “What goes up must come down”. The surplus has forced prices downward (Figures 2, 3 & 4)[10].

Figure 2. Brewers Supply Group (BSG) Hop Sale announcement

Source: Instagram post from February 12, 2024 on @craftbeerbrew

Figure 3. BSG Hop Sale price details[11]

Source: Brewers Supply Group web site[12]

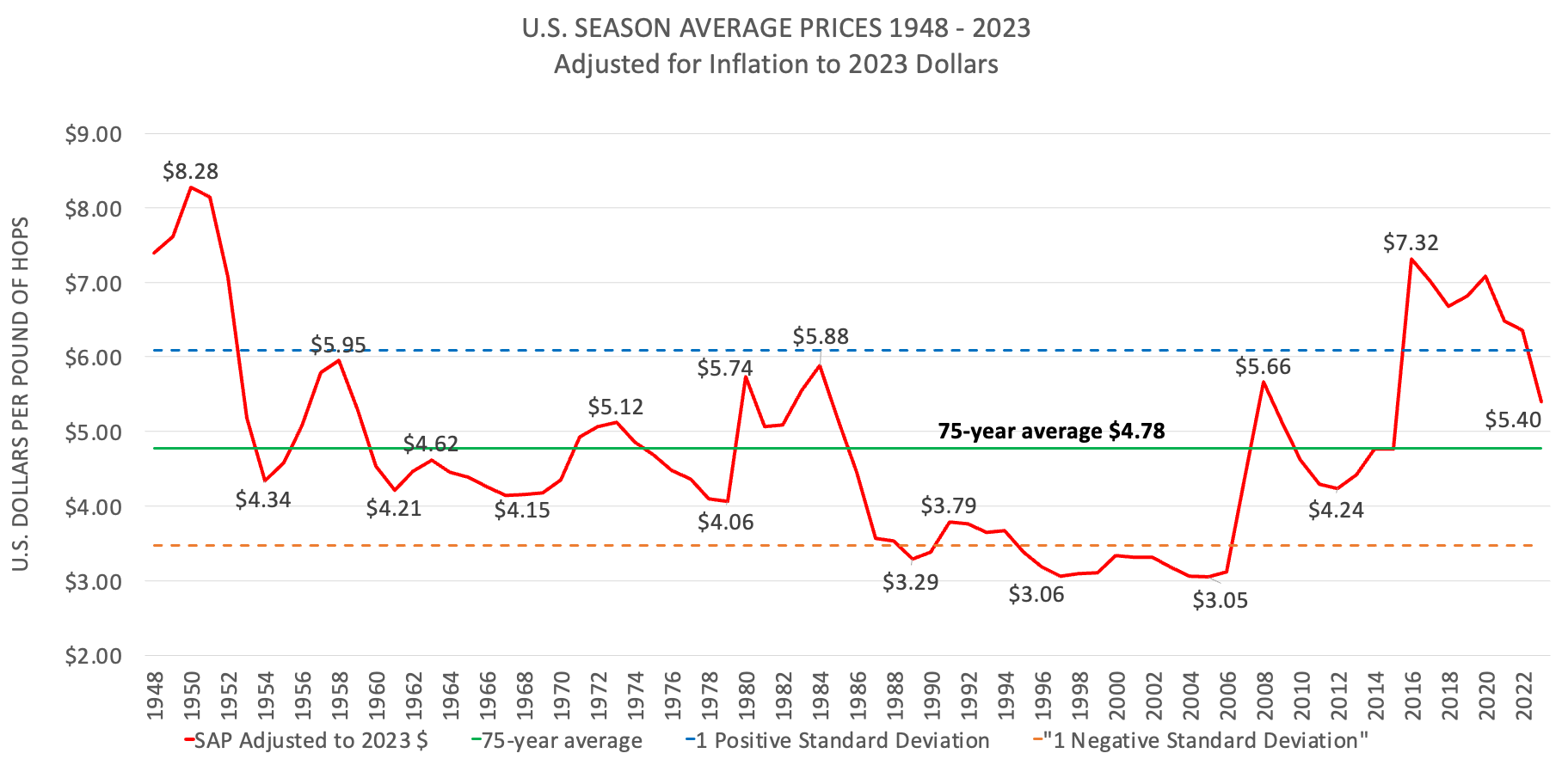

Figure 4. 75-year trend of USDA season average hop prices adjusted for inflation

Source: USDA NASS

Figures 2 and 3 represent the spot price reaction. Figure 4 is a mix of spot and contract prices across all varieties. For that reason, it is much less volatile and hides the most extreme price changes. Based on the prices above and the limited market activity, I believe spot prices have not yet found the bottom. Prior to the harvest, hops will head to the landfill to make space for the incoming 90-95 million pounds (40.8 – 43.1 MT.) in the U.S. from the 2024 crop.

BREWER PRO TIP: There are a lot of high alpha dual-purpose varieties available today. They’re older, but older hops are not worthless. Hauling hops to the landfill is not free. There may be opportunities for brewers looking for cheap bittering to source hops for the cost of shipping alone before they are discarded.

“If you’re going through hell, keep going.”

- Source unknown[13]

In German, the term for spot hops is freihopfen[14]. That translates in English to “free hops” in English. Hops going to the landfill is bad. Don’t worry. It’s not as bad as it sounds for the companies selling them. Inventory related losses can result in a refund of previously paid taxes or an offset of future tax liability for those companies. In layman’s terms, that means they may be able to recover what they paid for those hops in the form of fewer taxes paid. They lose their anticipated profits from the quantity they had to dump, but that’s not as bad as losing the entire investment.

BREWER PRO TIP:

In the American culture, bargaining is not as common as it is around the world. That doesn’t mean it doesn’t work. It doesn’t matter if the hops are fresh or old, brewers should bargain with the person selling them their hops. Between farmers and merchants there’s always a lot of haggling to reach a price. When I was a merchant, I was surprised by how few brewers sent back counteroffers. That resulted in some ridiculous pricing. Some brewers believe if they probe multiple merchants they can discover what the going prices are for the hops they need. When the answers come back close to one another, they believe that means that is what those hops cost. Tacit collusion in the industry enables every seller to offer similar prices regardless of their costs. If you want to understand how hop prices work, I explained it in my September 2022 article, “Who Sets Hop Prices … and How?” In a buyer’s market like 2024, it makes no sense for a buyer not to bargain.

… and now back to our regularly scheduled program: The big lie given today’s surplus is bankers agreeing to maintain the book value of aging inventory. Hop contracts are vital for the hop industry, but not for the reason brewers have been told. For more on that, read my August 2022 article called, “The Con in Hop Contracts”. This happens quietly behind the scenes to avoid triggering a mark to market event that would revalue existing inventory[15].

DIVISION

Now that craft beer has matured[16] and demand has declined[17], adding more proprietary varieties increases market division in a shrinking market. The Hop Breeding Company (HBC) brand loyalty will be difficult for its competitors to overcome … in part because they contributed to its strength[18]. The HBC global network effect via the companies with whom it shares common ownership (i.e., John I. Haas[19] and Yakima Chief Hops™[20][21]) gives the brand a powerful first mover advantage. It appears that’s not enough. Their aggressive tactics, some of which were shared with me by their competitors, appear designed to eliminate any and all from the market. They have the power to do that, but they need the brewers help.

Greater market division weakens the collective power of independent farmers and merchants trying to survive. It complicates their job by increasing the number of products they must offer. A significant number of American craft brewers … let’s say the smallest 9,500 … don’t have time to shop around with every merchant looking for somebody to take care of them. Buying hops is one of many jobs they have. The big merchants that control most of the world’s proprietary varieties know this. They leverage the value of their brands to sell both proprietary and public varieties. Farmers and merchants without access to proprietary varieties cannot compete for proprietary business. That creates a competitive disadvantage. It’s not hard to imagine 20-30% fewer hop farmers in the Pacific Northwest (PNW) by 2030. The independents will fight on searching for competitive advantages while hoping their neighbors walk away first.

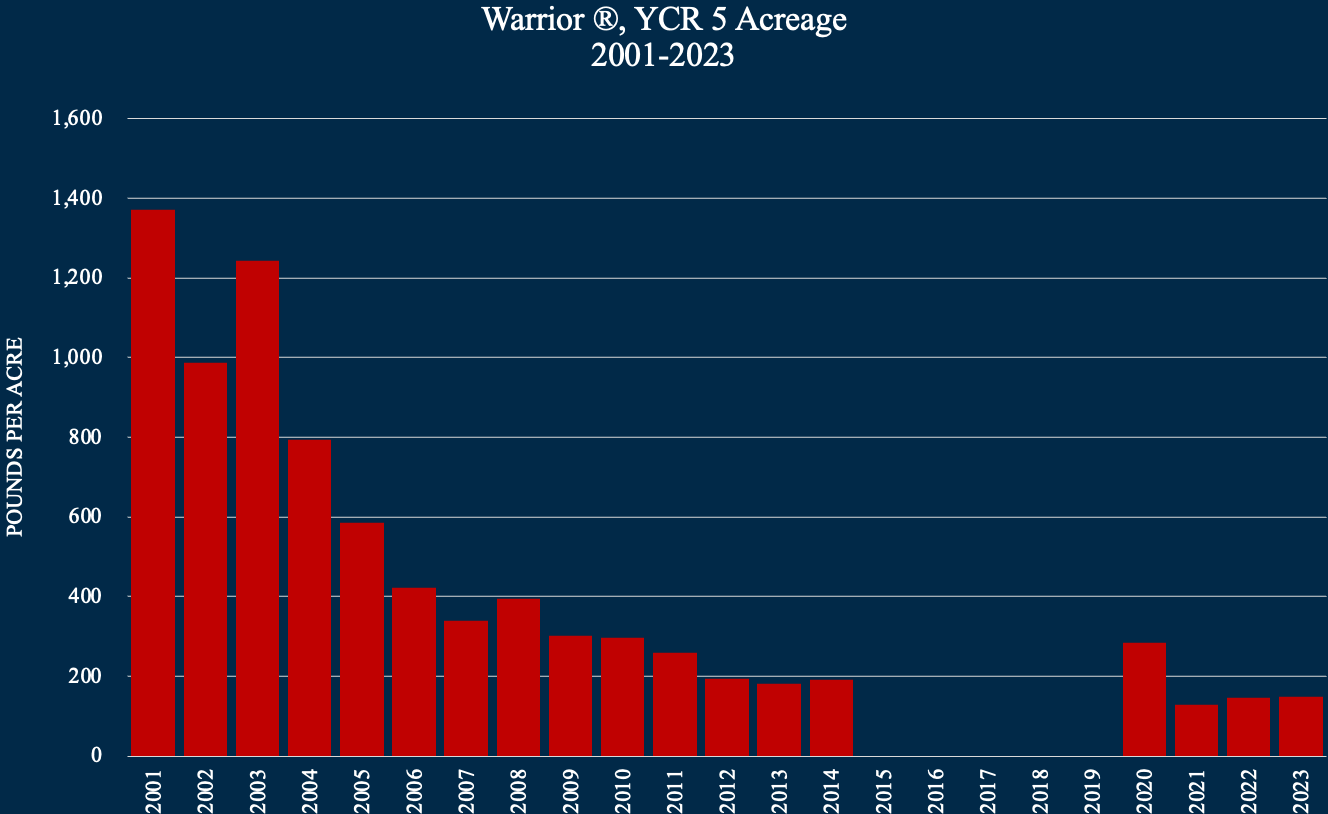

New proprietary hop varieties are seldom successful. Some great varieties enjoy limited success, but don’t meet the criteria for independent reporting by the USDA. Belma® is a good example[22]. Those hops end up in the “other” category. One example of this is Warrior® YCR 5. Prior to its release, the hype surrounding the variety was huge. Its owners claimed it was the 20/20 hop and would forever change the industry. History has proven that false, but it sold a lot of hops in the early years. Warrior® YCR 5 even vanished from the statistics between 2015 and 2019, at which time it was included in the other category. In 2023, there were 148 acres (59.91 ha.) of Warrior® YCR 5 in the U.S. (Figure 5).

Figure 5. U.S. Warrior® YCR 5 Acreage 2001-2023

Source: USDA NASS National Hop Reports 2001-2023

In 2023, the USDA released the acreage statistics for Hopsteiner’s Helios™ for the first time. At 1,509 acres (610.93 ha.), 2023 acreage resembles the first year of public data for the Warrior ® YCR 5 variety. Once again, the hype surrounding this variety is huge. As Warrior® YCR 5 acreage demonstrated, early brewer adoption is no indication of long-term success. Time will tell.

More proprietary varieties will bring increased market segmentation. For example, Helios™ is not available on the John I. Haas or YCH websites[23][24]. Another new variety, YQH 1320, also known as Elani™ Brand (YQH- 1320 cv.) was released in 2022. It’s a good example of a small merchant searching for a foothold in the market resulting in further market segmentation. In 2023, there were 61 acres (24.69 ha.) in Washington State and eight (3.23 ha.) acres in Idaho[25]. Based on its availability, it appears YQH has a distribution deal with John I. Haas[26][27]. It is also available through BSG[28] and the Hop Alliance[29]. As of April 30, 2024, it was not available on the Yakima Chief Hops™ or Hopsteiner web sites[30][31].

FUN FACT:

The address of the Yakima office for Yakima Chief Hops™ (YCH) is on DIVISION street. Of course, that’s a fun coincidence. They didn’t name the street. YCH is only the most recent hop merchant to call that address home. There is a good chance they will not be the last. Or … maybe it’s evidence we’re living in a simulation?

NUMBERS GAME

Charles Faram posted a statistic on their Instagram page in April 2024 that quantifies the scope of the proprietary variety situation for people who were not already aware (Figure 6).

Figure 6. Charles Faram Instagram post

Source: Instagram

What the post does not mention is that there are hundreds of thousands of potential hop varieties during the early stages of development. Most will be eliminated during the 10–15-year evaluation process[32][33][34][35]. According to Jason Perrault of Yakima Chief Ranches, hop breeding is a numbers game where fewer than 0.001% of the results show commercial potential[36].

In 1997, the last year before the USDA reported any proprietary varieties there were 13 hop varieties in production in the U.S. By 2023, that number had tripled. There were 39 that met the USDA criteria for individual reporting[37]. The trend implies that brewers are comfortable with Big Hop (i.e., a term I coined to describe the corporate ownership of the world’s hop supply).

The insatiable demand by craft brewers for proprietary varieties has led merchant/farmers to believe they must develop proprietary varieties to survive. They’re just following the money. By my count, there are at least 12 groups developing or managing new varieties in the U.S.[38]. That is significant in an industry, which in 2023 had 69 farmers[39]. Americans are not the only ones using proprietary varieties to fight for their survival. Similar programs exist in Germany[40], Slovenia[41], England[42], the Czech Republic[43], France[44], New Zealand[45], Australia[46], South Africa[47], Poland[48], Argentina[49], and Brazil[50] to name a few. That is a staggering amount of hop breeding!

DELAYED REACTION

Increased use of ultra-processed hop products reduce the need for hops due to their increased efficiency. The math is simple, but these create a challenge. I explained how varieties with increased alpha production flooded the market sending prices plummeting between 1980 and 2004 in my April 11, 2024 article, “Will Craft Beer Bring the Hopocolapyse?”. In theory, it would have been easy for farmers to correct for increased alpha efficiency by producing fewer acres in the 1980s, 1990s and 2000s. The increased alpha yield could have been easily calculated. In a free hop market, during a surplus, the decision to decrease production is delayed ensuring an extended period of overproduction[51][52].

Source: The New Yorker magazine cartoon online from May 2, 2024[53].

GAME FACE

Disrupting the industry with new proprietary varieties and advanced downstream products creates a Hobbesian Trap[54]. You might be more familiar with The Hobbesian trap stated this way: “They’re doing it, so we have to”, or “If we don’t do it, they will.” This has been the reasoning behind the development of nuclear weapons, the creation of deadly viruses through gain of function research and advances with artificial intelligence[55][56][57][58][59][60][61]. Proprietary varieties encourage brewer loyalty. Loyalty brings incredible value. Once one company headed down that path, the others had no choice (Figure 7).

Figure 7: Hop breeding program game theory chart.

This is the hop version of the prisoner’s dilemma[62]. The best option for the industry collectively would have been to remain in square 1. All players were equal. The market was not always good, but it was predictable. The lack of trust among the players made the move to proprietary varieties inevitable.

In squares 2 and 3, the HBC created a competitive advantage for itself[63]. The industry is on its way to square 4. Due to the number of players that will take some time. Creating and selling proprietary varieties is the perceived pathway to success. Case in point … On May 7, 2024, The Michigan Hop Alliance announced the availability of the second proprietary variety developed by the West Coast Hop Breeding on LinkedIn (Figure X).

Figure 8. Michigan Hop Alliance LinkedIn post.

Source: Michigan Hop Alliance LinkedIn page.

CONNECTION IS PROTECTION

If you haven’t heard of West Coast Hop Breeding, it’s a group of Oregon farmers who according to their web page exist “to ensure that Oregon hop growers have a sustainable future by developing varieties that thrive in Oregon’s unique soil and climate growing conditions”[64].

https://wchops.com

Not every merchant/farmer can afford a breeding program. The high failure rate combined with sporadic success makes them expensive. Alliances like West Coast Hop Breeding combat the HBC’s competitive advantage. Independent merchant/farmers that cannot afford their own breeding programs will move toward similar alliances hoping to develop a Unique Selling Proposition (USP).

Creating more proprietary varieties, however, won’t sustain the number of independent merchant/farmers that want to remain in business. There will be fewer independent merchant/farmers in five years.

Greater balance between proprietary and public variety usage would reduce the cartel’s power, provide opportunity to independent merchants and farmers and encourage competition-based pricing. It’s possible to put the genie back in the bottle. It’s a simple solution, but it is not easy. The industry is not headed that direction. The surplus today is a result of the overproduction of proprietary varieties. Nevertheless, following the acreage decreases of 2022 and 2023, proprietary acreage increased to record levels, 70.45% of American production in 2023[65][66][67]. I believe that trend will continue in 2024 (more on that in June).

If you’re made it this far in the article, thank you for reading! I hope you enjoy the perspectives you find here and find them valuable. If so, please consider subscribing or if you have already, maybe you can share it with somebody else who might find some value in it.

Proprietary hop variety development resembles the arms race between the U.S. and the U.S.S.R. It’s out of control[68]. The Cold War competition peaked in 1986 with 70,300 nuclear weapons worldwide[69][70]. They would still exist if it weren’t for a 1983 film called “The Day After”. An estimated 100 million Americans, including President Reagan, watched the movie, which depicted a nuclear holocaust in Kansas[71].

The President vowed such a thing would not happen on his watch. That changed the course of history[72]. Today there are 13,080 nuclear warheads, 130 times the amount necessary to make the Earth uninhabitable[73][74].

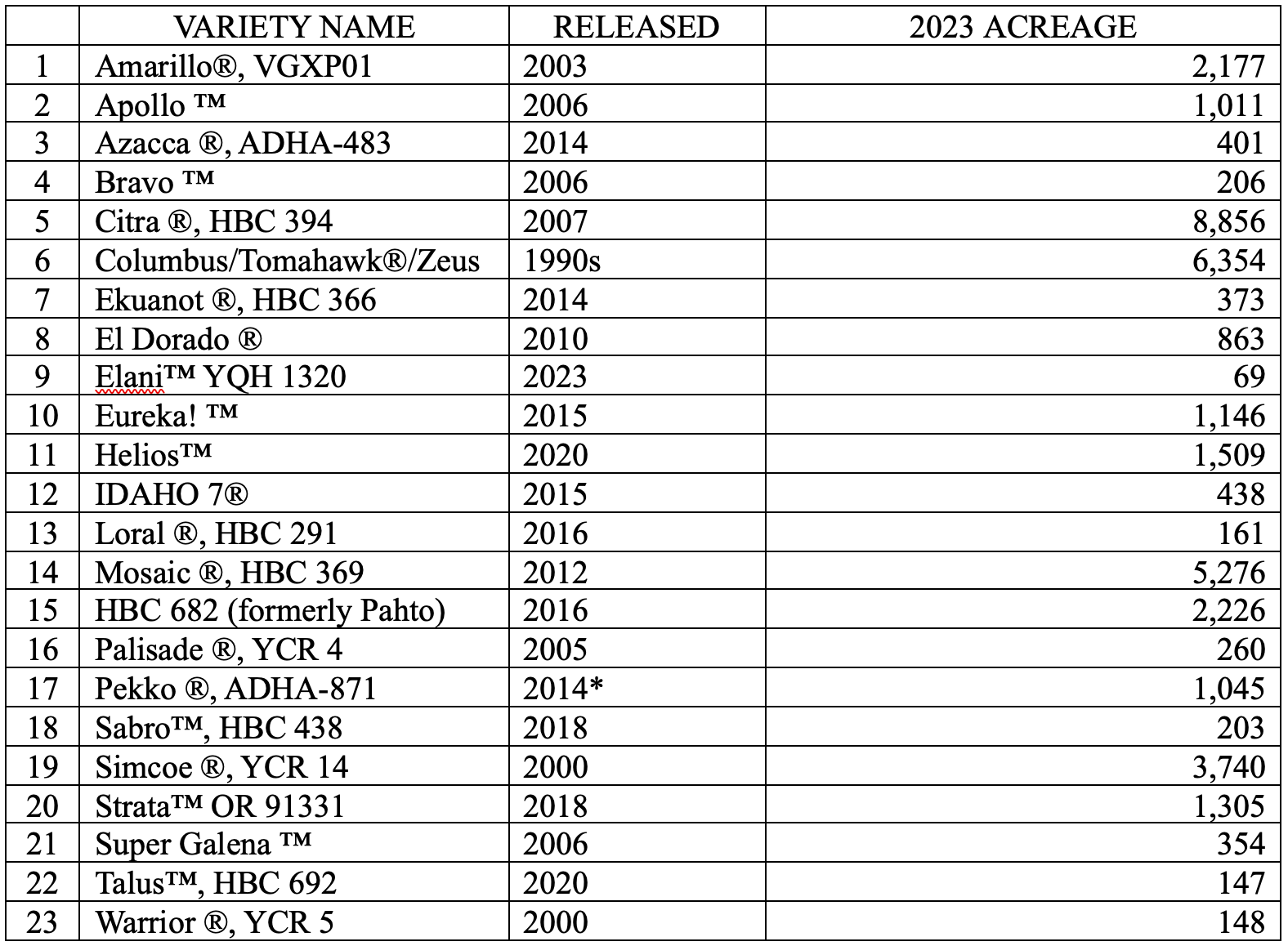

How many proprietary hop varieties are necessary before the hop industry reaches its “Day After” moment? 400? … 600? … 800? Cash cows like Citra® HBC 394 or Mosaic ®, HBC 369 rarely come along (Figure 9).

Figure 9. Proprietary hop varieties listed by the USDA, their release dates and 2023 acreage.

Source: 2023 USDA National Hop Report. Various sources for release date information[75][76][77][78][79][80][81][82][83][84][85][86][87][88][89][90][91][92][93][94].

*Patent filing date[95].

Between successes, countless varieties will enter the market. Breeding programs will soon notice the diminishing marginal return of each new variety they create. Well-financed private programs will use their war chest to continue beyond this point. Smaller programs will not be able to continue. There is no industry voice of reason to apply the brakes to runaway hop variety development. So long as breweries continue supporting proprietary varieties, companies will compete for hop supremacy.

Source: From the closing scene of the 1983 movie War Games

When the Brewers Association announced that beer production declined in 2023, it signaled the end of an era[96]. New varieties thrived during the craft boom because they helped capture part of a growing market. Today, proprietary varieties are a life preserver for those hoping to grab a bit of a shrinking market because in today’s market they is no other choice.

Based on their acreage, brewers seem to lack interest in new public varieties. That’s a mistake. Public varieties can restore a balance of power not possible in a proprietary world. Why should a brewer care about that so long as they can get the varieties they want? In a proprietary world, brewers will their hops from a handful of companies for premium prices that are never enough and increase every year. What chance for survival does an independent merchant or farmer with no USP have under the status quo?

Public varieties, on the other hand, support free market competition. I’ve only talked to one brewery purchasing agent who said he didn’t care if he was paying too much. He doesn’t work at the brewery anymore. Supporting public varieties supports independent merchants and farmers worldwide.

[1] https://www.nytimes.com/2024/05/03/technology/google-apple-amazon-meta-antitrust.html

[2] https://www.nytimes.com/2023/09/26/technology/amazon-ftc-lawsuit-antitrust.html

[3] https://hbr.org/2018/03/is-lack-of-competition-strangling-the-u-s-economy

[4] https://www.whitehouse.gov/cea/written-materials/2021/07/09/the-importance-of-competition-for-the-american-economy/

[5] https://www.brewersassociation.org/insights/hop-acreage-report/

[6] https://agriculture.ec.europa.eu/document/download/87ab6ec3-60fc-45b9-840a-70e6eed56469_en?filename=ext-eval-products-markets-final-report_2010_en.pdf

[7] https://www.deutscher-hopfen.de/HRI_2023_2024/S%20003_Editorial_HRI%2023-24_low.pdf

[8] https://www.hopsteiner.com/news/2023/11/guidelines-for-hop-buying-2023/

[9] https://brewingindustryguide.com/rightsizing-the-hop-market/

[10]https://go.bsgcraft.com/sale/?utm_source=craft+beer+brewing&utm_medium=digital&utm_campaign=hop+liquidation+cb&b+sponsored&utm_content=hops

[11] This is just a portion of the varieties available at these prices. More details were available at the link cited.

[12] https://go.bsgcraft.com/rs/566-YJV-184/images/BSG_HopSale_chart.pdf?version=0

[13] Falsely attributed to Winston Churchill according to the International Churchill Society: https://winstonchurchill.org/resources/quotes/quotes-falsely-attributed/

[14] https://www.lfl.bayern.de/mam/cms07/ipz/dateien/hopfen_Ökonomik_nachhaltigkeit.pdf

[15] https://corporatefinanceinstitute.com/resources/valuation/mark-to-market/

[16] https://www.brewbound.com/news/bart-watson-craft-market-isnt-maturing-it-has-matured/

[17] https://www.news5cleveland.com/craft-beer-production-has-declined-in-the-us-new-report-shows

[18] https://corporatefinanceinstitute.com/resources/management/first-mover-advantage/

https://www.hopbreeding.com

[20] https://www.yakimachief.com/our-company

[21] https://yakimachiefranches.com/history/

[22] https://hopsdirect.com/products/belma-leaf

[23] https://www.johnihaas.com/products/hops/

[24] https://www.yakimachief.com/commercial/hop-varieties.html?p=2

[25]https://www.nass.usda.gov/Statistics_by_State/Regional_Office/Northwest/includes/Publications/Hops/2023/hops1223.pdf

[26] https://www.johnihaas.com/products/hops/

[27] https://yakimavalleyhops.com/products/elani-hops

[28] https://bsgcraftbrewing.com/american-hops/

[29] https://hopalliance.com/products/elani-hop-pellets-2023?variant=40348072280198

[30] https://www.yakimachief.com/commercial/hop-varieties.html?product_list_limit=all

[31] https://www.hopsteiner.com/variety-data-sheets/

[32] https://www.goodbeerhunting.com/blog/2020/2/12/breeding-in-captivity-how-genetic-sequencing-is-changing-beers-main-ingredients

[33] https://yakimachiefranches.com/create/breeding/

[34] https://www.homebrewersassociation.org/how-to-brew/hbc-438-new-hop-variety-just-for-homebrewers/

[35] https://agsci.oregonstate.edu/hop-breeding/research-hop-breeding-and-genetics

[36] https://www.outsideonline.com/food/hops-craft-beer-popularity-future/

[37]https://www.nass.usda.gov/Statistics_by_State/Regional_Office/Northwest/includes/Publications/Hops/2023/hops1223.pdf

[38] My apologies if I missed anybody. There may be more. There are at least 12 groups.

[39] https://www.barthhaas.com/resources/barthhaas-report

[40] https://www.hvg-germany.de/en/

[41] https://www.ihps.si/en/hop-growing/hop-breeding/

[42] https://www.britishhops.org.uk/hop-breeding-2/

[43] https://www.chizatec.cz/en/

[44] https://www.beer-analytics.com/hops/dual-purpose/mistral/

[45] https://nzhops.co.nz/pages/innovation

[46] https://www.hops.com.au/hop-breeding-program/

https://zahops.com/#za-hops-descriptions

[48] https://polishhops.com/hop-breeding-programme/

[49] https://brauwelt.com/en/topics/raw-materials/642156-local-hop-varieties-from-patagonia#:~:text=Argentinian%20hops%20%7C%20In%20the%201980s,environment%20and%20obtaining%20better%20yields.

[50] https://www.sciencedirect.com/science/article/abs/pii/S1161030123002587

[51] https://web.archive.org/web/20220823014223id_/https://www.agriculturejournals.cz/publicFiles/156_2022-AGRICECON.pdf

[52] https://agriculture.ec.europa.eu/document/download/87ab6ec3-60fc-45b9-840a-70e6eed56469_en?filename=ext-eval-products-markets-final-report_2010_en.pdf

[53] https://www.newyorker.com/cartoons/daily-cartoon/thursday-may-2nd-technology-potential?utm_social-type=owned&utm_source=linkedin&utm_brand=tny&utm_medium=social

[54] https://www.kellogg.northwestern.edu/faculty/baliga/htm/hobbesiantrap.pdf

[55] https://static.googleusercontent.com/media/research.google.com/en//pubs/archive/46290.pdf

[56] https://www.congress.gov/117/meeting/house/114270/documents/HHRG-117-GO24-20211201-SD004.pdf

[57] https://www.cnn.com/2024/03/09/politics/us-prepared-rigorously-potential-russian-nuclear-strike-ukraine/index.html

[58] https://theintercept.com/2021/09/09/covid-origins-gain-of-function-research/

[59] https://www.reuters.com/world/nukes-space-what-have-russia-united-states-said-2024-02-21/

[60] https://www.state.gov/report-on-the-status-of-tactical-nonstrategic-nuclear-weapons-negotiations/

[61] https://www.forbes.com/sites/steveforbes/2023/03/30/laboratories-are-still-performing-gain-of-function-research-on-viruses-more-dangerous-than-covid-19/?sh=27d4bf722259

[62] https://www.kellogg.northwestern.edu/faculty/baliga/htm/hobbesiantrap.pdf

[63] This is an oversimplified example of the real situation in the hop industry in which there are today at least 11 variety development programs.

https://wchops.com

[65] https://brewingindustryguide.com/the-next-hop-market-correction/

[66] This does not count any proprietary varieties that are included in the “other” or “experimental” category. The true percentage of proprietary varieties produced in the U.S. is higher.

[67]https://www.nass.usda.gov/Statistics_by_State/Regional_Office/Northwest/includes/Publications/Hops/2023/hops1223.pdf

[68] https://www.amazon.com/Nuclear-War-Scenario-Annie-Jacobsen/dp/0593476093/ref=sr_1_1?dib=eyJ2IjoiMSJ9.btPtnXTnYHlwft9pjcT5zGPQpUqY-9DdbydH1e2mao4MJ21BZnf7bXQPrsUA4RHSq7r7Ac1-497gzvTG46lje0INMt4ewxetRRu5zrSvCUZnLtGFXM_hrX85dq1MgWwLxQIyBAAzroX6HhTwXZq2uOft8gyV7TVXlJw5zk0H4b1x1awdt2U-hkP8NuPQqQbfWZFtf2_Dhn3FxnWfK78Ov1bzlHlbrX6pG20R38clFV8.s7pHtxxfTaOWYCpBN6GtM4W_0DbK0oR6dzRh-InXMnM&dib_tag=se&keywords=Annie+Jacobsen+nuclear+war&qid=1715154194&sr=8-1

[69] https://responsiblestatecraft.org/2023/08/02/oppenheimer-and-the-birth-of-the-nuclear-industrial-complex/

[70] https://fas.org/initiative/status-world-nuclear-forces/

[71] https://www.imdb.com/title/tt0085404/

[72] https://time.com/6337667/day-after-tomorrow-cold-war-essay/

[73] https://www.chathamhouse.org/2023/06/nuclear-governance-model-wont-work-ai

[74] https://worldpopulationreview.com/country-rankings/nuclear-weapons-by-country

[75] https://www.barthhaas.com/hops-and-products/hops/amarillor-vgxp01-cv

[76] https://www.hopslist.com/hops/bittering-hops/apollo/

[77] https://www.geterbrewed.com/azacca-t90-hop-pellets-usa/

[78] https://brewculture.com/products/el-dorado®-cryo-hops®

[79] https://dcbeer.com/2016/11/26/hop-harvest-qa-with-hopsteiner/

[80] https://hopheadfarms.com/hops/idaho-7-hops/#:~:text=If%20so%2C%20you've%20likely,since%20its%20release%20in%202015.

[81] https://beermaverick.com/hop/bravo/

[82] https://www.stonebrewing.com/beer/special-releases/stone-loral-dr-rudis-inevitable-adventure-double-ipa#:~:text=Loral%20hops%20were%20released%20in,of%20our%20brewers'%20favorite%20varieties.

https://www.hopbreeding.com

[84] https://brulosophy.com/2020/01/02/the-hop-chronicles-ctz-2018/

[85] https://yakimavalleyhops.com/products/ekuanot-hop-pellets

[86] https://www.brewersjournal.ca/2020/08/25/hop-breeding-company-announces-commercial-release-of-talus-brand-hbc-692-hop-variety/

[87] https://www.linkedin.com/posts/hopsteinerhops_the-history-of-helios-since-2006-activity-7167564734462935040-4Puq/

[88] https://beermaverick.com/hop/strata/

[89] https://patents.justia.com/patent/20170127588

[90] https://www.twobeerdudes.com/hops/profile/146/super_galena

[91] https://yakimavalleyhops.com/products/sabro-hop-pellets

[92] https://yakimavalleyhops.com/products/simcoe-hop-pellets

[93] https://patentimages.storage.googleapis.com/24/89/53/7bcb5adf486912/USPP15663.pdf

[94] https://www.beer-analytics.com/hops/bittering/warrior/#:~:text=Warrior%20hops%20are%20a%20unique,among%20commercial%20and%20homebrewers%20alike.

[95] No release date is publicly available online. The patent filing date is the most reliable date associated with the release of the variety. https://patentimages.storage.googleapis.com/f3/1c/05/283598704477f5/USPP27779.pdf

[96] https://www.brewersassociation.org/statistics-and-data/national-beer-stats/